Typical Answers To Home Mortgage Questions

Article by-McManus HoffmanOwning a home is a reason for pride. The process of getting a home does require that most people take out a mortgage. Obtaining a mortgage can be confusing and overwhelming. Keep reading for information on taking out home mortgages.

Understand your credit score and how that affects your chances for a mortgage loan. Most lenders require a certain credit level, and if you fall below, you are going to have a tougher time getting a mortgage loan with reasonable rates. A good idea is for you to try to improve your credit before you apply for mortgage loan.

Before applying for a mortgage, pay down your debts. Lenders use a debt to income ratio to verify that you are able to afford a mortgage. A general rule of thumb is 36 percent of your gross income should be available to pay all of your monthly expenses, including your mortgage payment.

Regardless of how much of a loan you're pre-approved for, know how much you can afford to spend on a home. Write out your budget. Include all your known expenses and leave a little extra for unforeseeable expenses that may pop up. Do not buy a more expensive home than you can afford.

If you're thinking of getting a mortgage you need to know that you have great credit. Lenders review credit histories carefully to make certain you are a wise risk. Do what you need to to repair your credit to make sure your application is approved.

If your mortgage spans 30 years, think about chipping an additional monthly payment. This will help pay down principal. If you pay an additional amount on a routine basis, your can be paid off faster and your total interest liability can be a lot less.

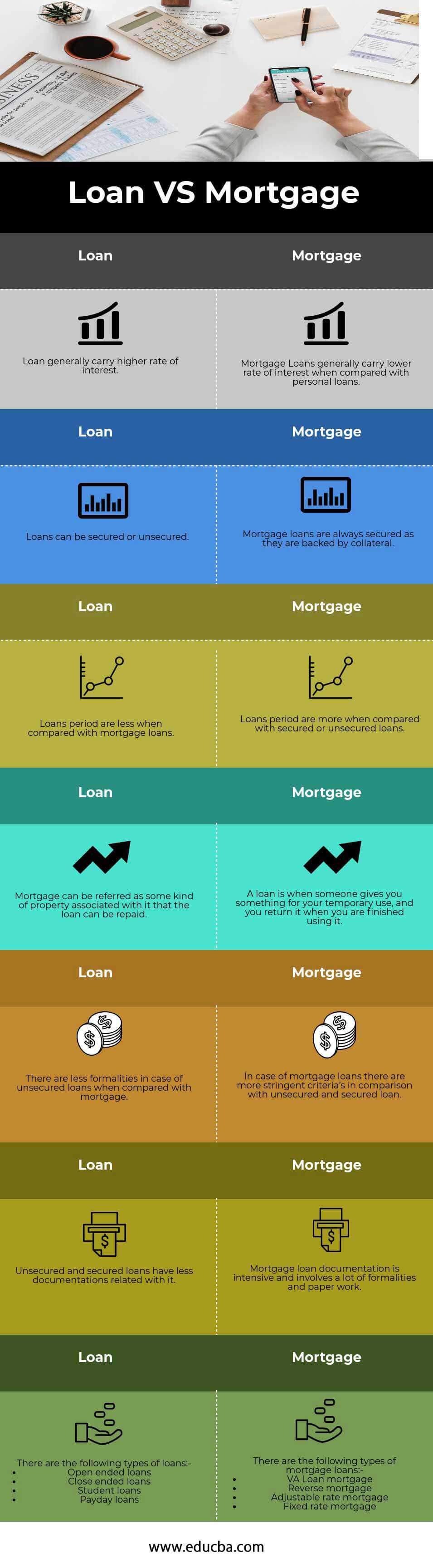

Learn about the three main types of home mortgage options. The three choices are a balloon mortgage, a fixed-rate mortgage, and an adjustable-rate mortgage (ARM). Each of these types of mortgages has different terms and you want to know this information before you make a decision about what is right for you.

When rates are near the the bottom, you should consider buying a home. If you do not think that you will qualify for a mortgage, you should at least try. Having your own home is one of the best investments that you can make. Quit throwing away money into rent and try to get a mortgage and own your own home.

Do not accept https://www.chase.com/personal/investments/online-investing that is variable. If the economy experiences ups and downs, so will your mortgage. This could have a very negative impact on your finances. This may make it too hard for you to pay for your home, which is something you're probably not wanting to have happen.

Think about your job security before you think about buying a home. If you sign a mortgage contract you are held to those terms, regardless of the changes that may occur when it comes to your job. For example, if you are laid off, you mortgage will not decrease accordingly, so be sure that you are secure where you are first.

You should have the proper paperwork ready in advance for a lender. just click the up coming internet page well prepared. You'll need a copy of your pay stubs going back at least two paychecks, your last year's W-2 forms and a copy of last year's tax return. You'll also need your bank statements. Get those together before the lender asks.

Pay off more than your minimum to your home mortgage every month. Even $20 extra each month can help you pay off your mortgage more quickly over time. Plus, it'll mean less interest costs to you over the years too. If you can afford more, then feel free to pay more.

Look into credit unions. There are many options for obtaining financing and credit unions have their strengths. Often credit unions will hold mortgages in their private portfolio. Banks and other financial institutions routinely sell mortgages to other holding companies. This could result in your loan changing hands multiple times over its lifetime.

Pay your mortgage down faster to free up money for the future. Pay a little extra each month when you have some extra savings. When you pay the extra each month, make sure to let the bank know the over-payment is for the principal. You do not want them to put it towards the interest.

If you can, you should avoid a home mortgage that includes a prepayment penalty clause. You may find an opportunity to refinance at a lower rate in the future, and you do not want to be held back by penalties. Be sure to keep this tip in mind as you search for the best home mortgage available.

If you have a lot of open credit cards, consider paying them off and closing the accounts before applying for a home loan. Many lenders look negatively upon the overuse of credit. So, by closing your credit card accounts, you can show that you are a worthy credit risk for the lender.

Think about accepting a mortgage for a shorter term. The less time it takes you to pay off your home, the less interest you will pay. Of course, you will pay higher monthly payments on a fifteen year mortgage than on a twenty year mortgage, but in the long run you will save many thousands of dollars. Additionally, owning your home outright will give you tremendous peace of mind.

If you don't agree with the lender's assessment made on your prospective home, you can get a second opinion. Of course, you can't tell the original lender to hire another appraisal, but you can apply to another lender. Then you can hope that you get a more favorable assessment from their appraiser.

As was stated in the introductory paragraph of this article, the mortgage financing process is very complicated. It can seem indecipherable to a real estate novice. The key to financing a great mortgage that allows you to buy the home of your dreams is to educate yourself on the mortgage process. Study the mortgage tips and advice in this article very carefully.